The economic impact of climate change is becoming increasingly evident as rising global temperatures threaten to disrupt markets and economies worldwide. Recent studies indicate that every increment of warming could result in drastic declines in global GDP, with potential losses peaking significantly within just a few years post-temperature increase. As climate change economics evolves, economists are revisiting their models to reflect these alarming projections, which are now believed to be up to six times more severe than earlier estimates. The implications of these findings extend beyond mere statistics; they highlight the urgent need to reconsider the social cost of carbon and advocate for effective decarbonization strategies that can yield substantial economic benefits. Understanding the intricate relationship between climate change and economic stability is crucial as we navigate the complex landscape of environmental policy and market dynamics.

The financial ramifications of environmental transformations are increasingly a focal point for researchers and policymakers alike. Known as the economic consequences of climate fluctuations, these issues emphasize how changing weather patterns can lead to significant reductions in productivity and overall economic health. As the global economy faces unprecedented challenges driven by rising temperatures and extreme weather events, the discussion surrounding climate change-related economic forecasts becomes paramount. Terms like climate change economics and GDP decline due to climate shifts illustrate the urgent need to adapt our strategies in response to these potentially damaging phenomena. Exploring the extensive implications of these environmental changes is essential to forge pathways that combine economic growth with sustainable practices.

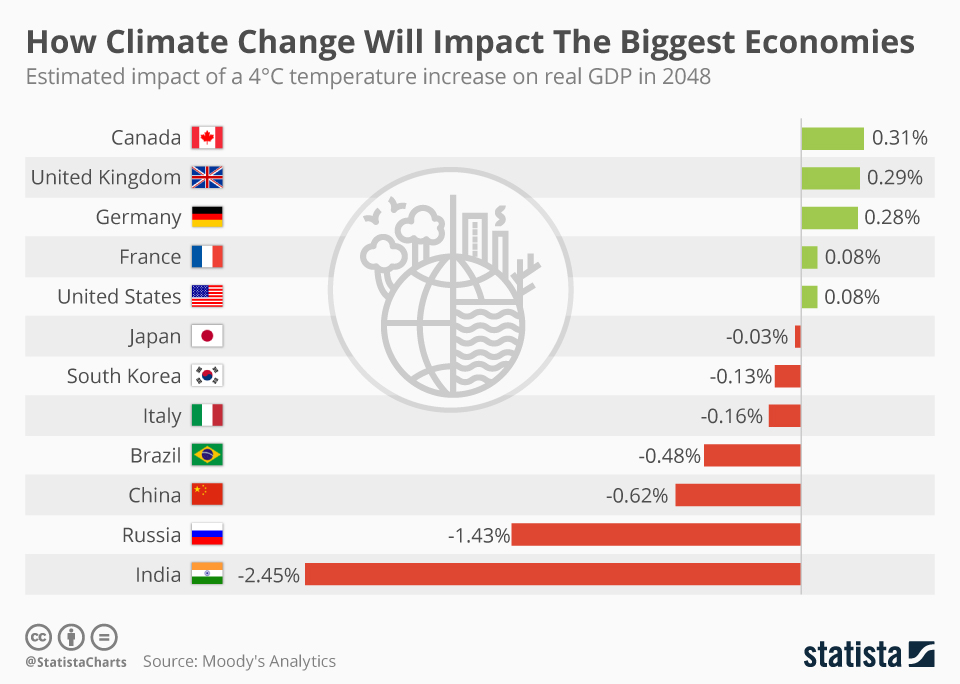

The Growing Economic Toll of Climate Change

Climate change is imposing significant economic burdens globally, and recent studies suggest that the financial impact is far greater than previously estimated. As temperatures continue to rise, macroeconomists have reevaluated the potential damages, revealing a staggering forecast that projects a 12% decline in GDP for every additional degree of warming. This revised prediction underscores the urgent need for policymakers to address the economic dimensions of climate change, beyond merely viewing it as an environmental crisis. Through this lens, the economic impact of climate change becomes a pressing issue that intertwines with public health, infrastructure resilience, and overall societal well-being.

The analysis of climate change’s economic toll extends to various sectors, illustrating how industries face increased risks from climate-induced events such as extreme weather. For instance, agriculture is particularly vulnerable, as shifting climate patterns can lead to crop failures and higher food prices. Moreover, the service sector, which relies heavily on consumer behavior, can experience fluctuations as public confidence shifts due to climate-related disasters. Understanding these economic interdependencies is crucial for developing a comprehensive strategy that effectively mitigates not only the environmental damage but also the financial ramifications that come with it.

Decarbonization and Its Economic Advantages

Decarbonization strategies are becoming imperative for mitigating the adverse effects of climate change on the economy. The recent study indicated that the social cost of carbon could be as high as $1,056 per ton, which starkly contrasts with other estimates that suggest much lower values. This discrepancy highlights the urgency for robust decarbonization policies that take into account the long-term economic benefits of reducing carbon emissions. Investing in clean technology and renewable energy not only contributes to a more sustainable environment but also has the potential to generate substantial economic savings in the face of escalating climate change costs.

Furthermore, transitioning to a decarbonized economy could lead to significant job creation and technological innovation. Sectors focused on renewable energy, energy efficiency, and sustainable agriculture can stimulate economic growth while reducing carbon footprints. Policymakers are increasingly recognizing that the benefits of decarbonization extend beyond environmental sustainability; they encompass economic resilience and enhanced productivity. When approached with a comprehensive plan, decarbonization can serve as a pathway out of economic stagnation caused by climate impacts, making it a win-win solution for both the planet and prosperity.

Understanding the Social Cost of Carbon

The social cost of carbon represents a critical metric for assessing the economic implications of greenhouse gas emissions. Current estimates that place it at $1,056 per ton highlight the pressing need for policymakers to incorporate climate change’s extensive impacts into economic planning. This figure suggests that the economic ramifications of carbon emissions are far-reaching, affecting everything from public health to disaster preparedness. Understanding the social cost of carbon is crucial for creating effective climate policies that not only mitigate environmental harm but also promote economic stability.

By recalibrating the social cost of carbon based on comprehensive data that includes global temperature effects, researchers like Bilal and Känzig have shed light on how high the stakes are. The implications for industries and consumers alike are profound; acknowledging this cost can inform better decision-making in both the private and public sectors. Moreover, integrating the social cost of carbon into economic analyses allows for more nuanced predictions about future GDP losses, helping to advocate for stronger climate action that can secure economic survival in the face of ongoing climate changes.

The Link Between Climate Change and GDP Decline

There is a stark correlation between rising global temperatures and GDP decline, emphasizing the pressing need for comprehensive climate action. New studies predict that every increase of 1°C may lead to a significant 12% decrease in global GDP within a matter of years. Such alarming figures necessitate immediate attention from economists and policymakers who need to understand the broader economic implications of ignoring climate projections. The message is clear: failing to address climate change not only jeopardizes the environment but also threatens economic stability on a global scale.

Moreover, the detrimental effects on GDP are compounded by the increasing frequency of extreme weather events. These events disrupt economic activities, damage infrastructure, and displace populations, leading to substantial productivity losses. Recognizing that climate change is an economic issue rather than solely an environmental one is essential for fostering bipartisan support for climate policies. By framing climate action in economic terms, stakeholders can better engage with those hesitant about environmental regulations, ultimately paving the way for stronger action against climate-induced economic fallout.

Extreme Weather and Productivity Losses

Extreme weather events are becoming increasingly common due to climate change, resulting in notable productivity losses and economic disruptions. Research indicates that as global temperatures rise, the frequency of heatwaves, storms, and flooding increases, leading to significant downturns in productivity across various sectors. For example, industries reliant on outdoor labor, like agriculture and construction, are particularly vulnerable to these disruptions, as adverse weather conditions can halt operations and yield devastating economic consequences. Understanding the relationship between extreme weather and productivity is essential for businesses and governments alike to bolster resilience against future climate impacts.

In addition to immediate impacts on labor, the long-term consequences of extreme weather can create systemic risks within economies. The costs associated with repairing damaged infrastructure, restoring supply chains, and supporting displaced populations can strain public resources and slow economic recovery. Furthermore, as these events become more frequent, uncertainty in local economies can deter investment and stifle growth. Recognizing the interconnection between climate change, extreme weather, and economic productivity is vital for formulating adaptive strategies that promote resilience and ensure sustainable economic growth.

Investing in Climate-Resilient Solutions

To safeguard future economic stability, investing in climate-resilient solutions is essential. This investment represents a proactive approach to mitigating the risks associated with climate change while promoting long-term economic prosperity. Enhancing infrastructure to withstand extreme weather, developing early warning systems for natural disasters, and implementing sustainable agricultural practices can offer substantial economic returns in the face of growing climate threats. By prioritizing these initiatives, governments and organizations position themselves to not only protect their existing assets but also facilitate future growth.

Moreover, fostering innovation in climate-resilient technologies can drive economic opportunities, create new jobs, and enhance the overall productivity of economies. As businesses begin to incorporate sustainability into their core operations, they not only mitigate risks but also tap into the growing demand for environmentally friendly products and services. Transitioning towards a greener economy is increasingly viewed as an essential strategy for maintaining competitiveness in a rapidly changing global market. Therefore, investing in climate-resilient solutions is not just beneficial for the environment; it is a sound economic decision that can yield significant long-term benefits.

The Role of Policy in Climate Economics

Effective policy enforcement is crucial for addressing the economic implications of climate change. Governments play a vital role in shaping the economic landscape through regulations that either promote or hinder sustainability efforts. Policymakers must prioritize climate-conscious economic strategies that reflect the true costs of carbon and incentivize decarbonization. The Inflation Reduction Act, for instance, exemplifies how targeted interventions can lead to significant drops in the social cost of carbon while fostering economic growth. By designing policies that integrate environmental concerns with economic goals, states can set the groundwork for a resilient future.

Furthermore, crafting policies that encourage public and private investments in renewable energy can reduce dependence on fossil fuels and decrease emissions over time. These policies can span multiple sectors, from transportation to manufacturing, ensuring a comprehensive approach to climate economics. Engaging stakeholders across various levels, including communities, businesses, and environmental organizations, can help foster collaboration and amplify the effectiveness of these policies. Ultimately, the hallmark of forward-thinking climate economics lies in recognizing the necessary intersection of environmental sustainability and economic viability.

Long-term Projections for Climate Change and Economy

The long-term projections for climate change’s impact on the economy raise serious concerns about future economic stability. If current trends continue, researchers predict that we could experience a 50% reduction in output and consumption resulting from an additional 2°C rise in global temperatures. Such a scenario would not only create unprecedented economic challenges but also potentially result in a prolonged recession-like atmosphere globally. The ramifications of a sustained downturn of this magnitude could fundamentally reshape economic systems, underscoring the urgent need for immediate action to mitigate climate change.

In order to craft informed climate policies, it is essential to analyze these long-term projections and incorporate them into economic planning. For instance, decisions regarding resource allocation for infrastructure, workforce development, and disaster preparedness need to reflect these potential outcomes. Moreover, integrating climate projections into economic forecasting offers valuable insights into potential risks and opportunities that could shape various sectors in the coming decades. By strategically planning for these outcomes, policymakers can develop robust frameworks that protect both the environment and the economy from the looming threats posed by climate change.

Harnessing Technological Innovations for Sustainable Growth

Technological innovations are poised to play a pivotal role in combating climate change and fostering sustainable economic growth. Advancements in renewable energy technologies, such as solar and wind power, are decreasing dependency on fossil fuels while simultaneously creating burgeoning job markets. Furthermore, innovative practices in energy efficiency and resource management can significantly reduce operational costs across industries. Harnessing these technologies not only aids in cutting greenhouse gas emissions but also represents a robust strategy for stimulating long-term economic growth, particularly as consumers increasingly demand eco-friendly products.

Emphasizing the development and adoption of climate-friendly technologies also opens the door for investments in research and development. As companies and governments commit resources towards exploring new solutions, they not only enhance sustainability efforts but also drive economic revitalization in communities. By fostering an environment that encourages innovation, we can empower businesses to adapt to changing regulations and consumer expectations, thus creating a dynamic marketplace that thrives on sustainability principles. The interplay between technology and economic growth illustrates a promising path towards a resilient future, where efforts to mitigate climate change can result in tangible economic benefits.

Frequently Asked Questions

What is the economic impact of climate change on global GDP?

The economic impact of climate change is substantial, with studies indicating that every additional 1°C rise in global temperatures could lead to a 12 percent decline in global GDP. This forecast shows that the costs of climate change are significantly underestimated compared to previous estimates, emphasizing the urgent need for climate action.

How do rising global temperatures affect economic productivity and spending?

Rising global temperatures adversely affect economic productivity and spending by increasing the frequency and severity of extreme weather events. As temperatures rise, productivity can decline due to heat stress and disruptions to infrastructure, thus greatly impacting the overall economic performance and leading to predictive declines in GDP.

What are the social costs associated with carbon emissions in climate change economics?

In climate change economics, the social cost of carbon is a key measure that estimates the economic damages associated with an increase in carbon emissions. Recent research has calculated this figure as high as $1,056 per ton globally, significantly higher than earlier estimates, underscoring the importance of effective policies for emissions reduction and decarbonization.

What are the benefits of decarbonization in light of climate change’s economic impacts?

Decarbonization offers substantial benefits by reducing the long-term economic impact of climate change. It can enhance economic resilience, prevent catastrophic GDP losses from extreme weather, and ultimately lead to higher economic growth. Studies demonstrate that the cost-benefit analysis for decarbonization strongly favors investment in renewable technologies, especially in large economies like the U.S. and EU.

How does the economic impact of climate change correlate with extreme weather events?

The economic impact of climate change is closely linked to the increasing frequency of extreme weather events, which are projected to rise with global temperature increases. These events can disrupt economic activities, damage infrastructure, and reduce productivity, leading to significant economic losses and challenges in forecasting GDP performance in a changing climate.

What should policymakers consider regarding climate change economics and GDP forecasts?

Policymakers should consider the revised economic forecasts regarding climate change, which indicate that neglecting climate impacts could result in substantially larger economic losses than previously estimated. Effective adaptation strategies and investments in decarbonization can mitigate these losses, making climate action a priority for sustainable economic growth.

| Key Point | Details |

|---|---|

| The Economic Toll of Climate Change | New study forecasts economic impact to be six times higher than previous estimates. |

| Temperature Rise Impact | Every additional 1°C rise in global temperatures results in a 12% decline in global GDP. |

| Extreme Weather Events | Global warming correlates with increased extreme weather events that adversely affect the economy. |

| Economic Modeling | Use of global temperature data from the past 120 years to project economic outcomes. |

| Social Cost of Carbon | New estimates suggest a social cost of $1,056 per ton of CO2, significantly higher than previous estimates. |

| Policy Implications | Decarbonization efforts are deemed beneficial and economically viable, particularly in large economies. |

Summary

The economic impact of climate change is becoming increasingly evident, as recent studies suggest that the costs could be far higher than earlier projections. With every additional degree of temperature rise forecasted to reduce global GDP by 12%, the potential for significant loss is alarming. Moreover, extreme weather events related to climate change further complicate economic forecasting and growth. This necessitates urgent policy shifts towards decarbonization, which not only mitigates climate risks but also presents a lucrative opportunity for economic stability. As such, the potential for a 50% reduction in global output under higher temperature scenarios calls for immediate attention and action.